GROM and the 40% rule

I came across the 40% rule this week after reading a Hacker News thread on Twilio's IPO filing.

An oft criticism of SaaS companies is they don’t make money. The 40% rule is a tidy way of explaining why this is okay (during early years) for the sake of growth. (For a deeper dive on the SaaS model, it’s revenue recognition schedule, and what this means for profits, check out this primer from A16Z’s Scott Kupor and Preethi Kasireddy.)

The 40% rule:

Annual revenue growth rate + operating margin should equal 40%.

If you’re above 40%, even better.

In other words, if you’re growing at 40% a year, you should be breaking even (or better) on operating margin. If you’re growing at 100% a year, you can afford to operate at an operating margin loss of 60%.

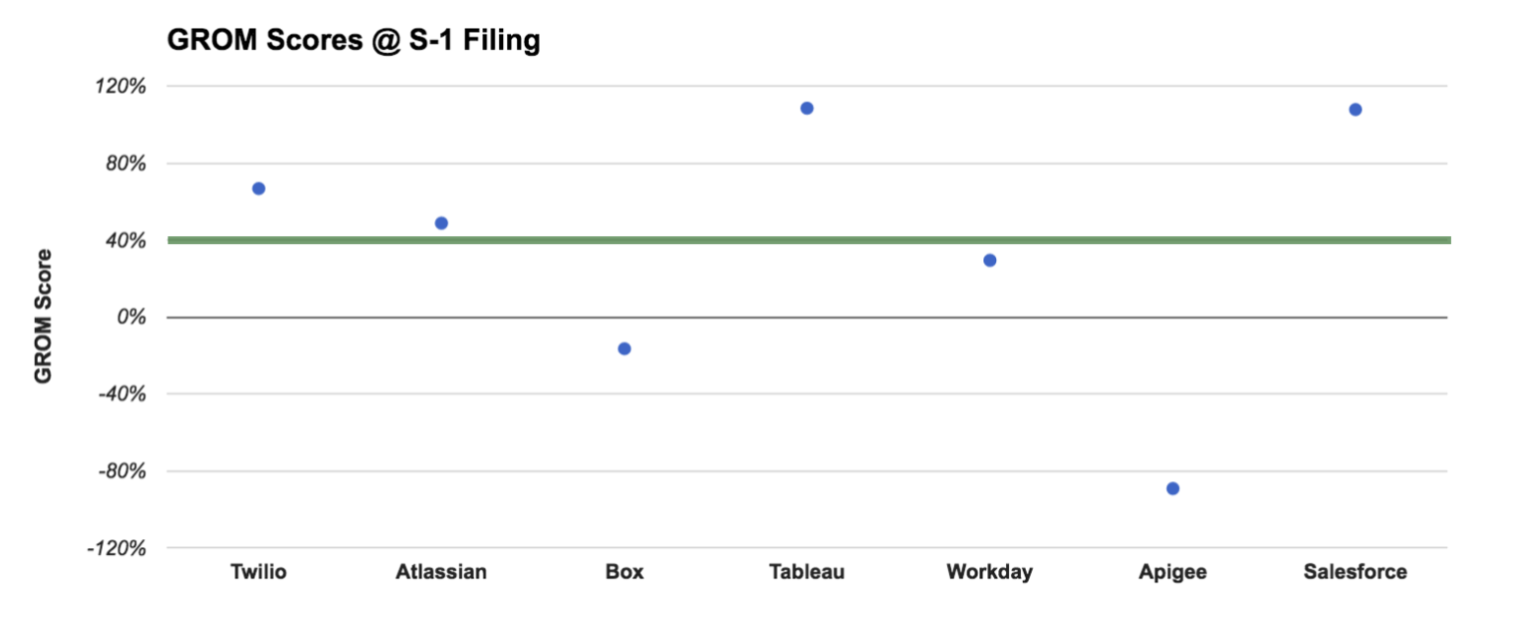

Here’s a number of well-known SaaS companies and their GROM (growth rate + operating margin) scores at their S-1 filing date.

GROM balances growth rate and operating margin. As an example, a company like Atlassian that spread via word of mouth (lower marketing costs and improved operating margin) is rewarded; conversely, Box, despite a growth rate that’s double that of Atlassian, is punished because of an operating margin deficit that outpaces the growth rate it serves.

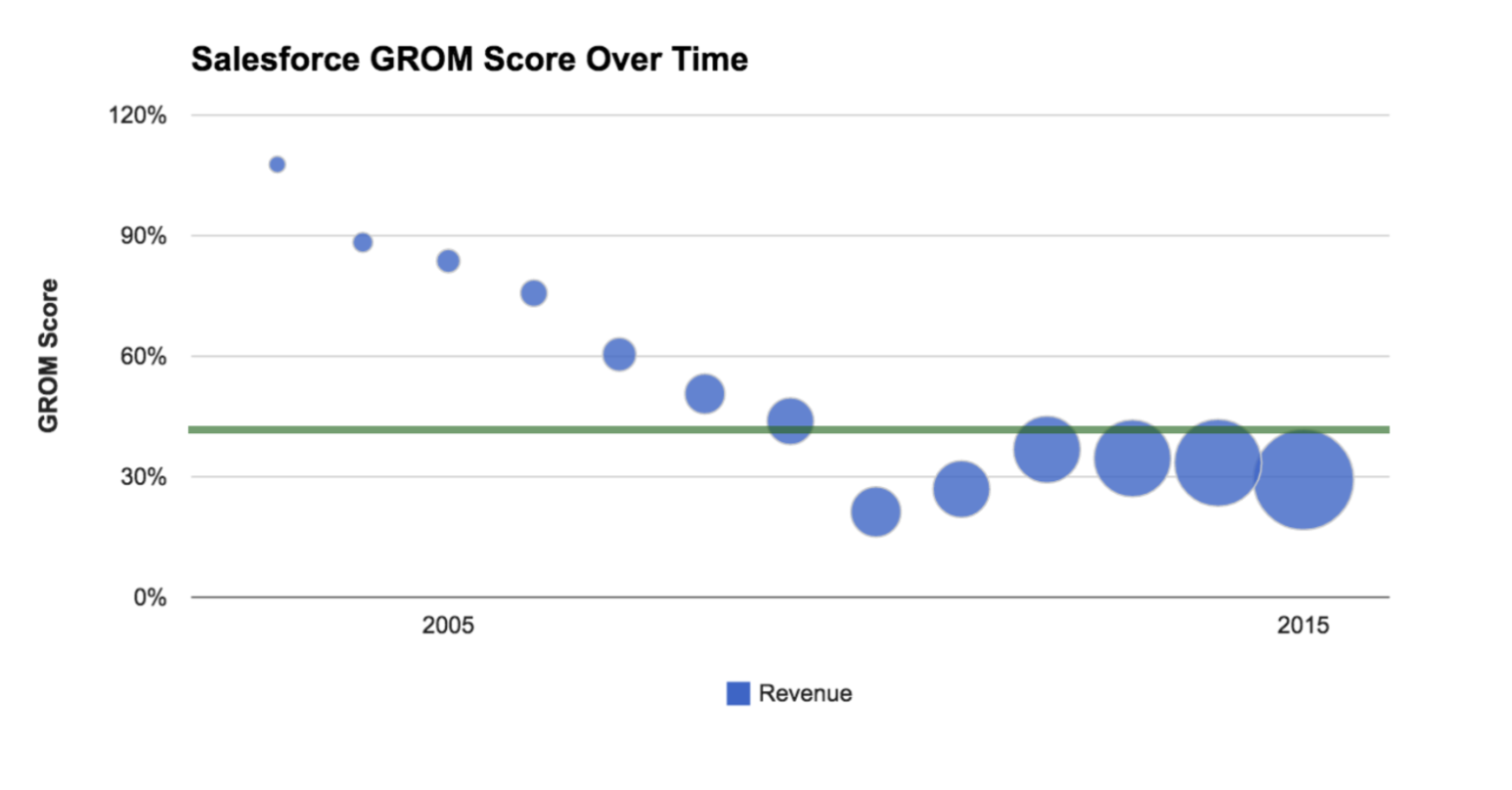

The 40% rule also prescribes the long-term arc for SaaS companies, in which early years are spent in hyper growth mode, losing money, and later years are spent optimizing profits after the growth curve has started to flatten.

As an example, here’s Salesforce’s GROM score plotted since they went public in 2003.

Next time you’re wondering how a SaaS IPO might fare, try GROM. The sweet spot is 40%.